Posted on: January 1st, 2022

If you’re like lots of business owners, you’re looking out for more than just the financial health of your company. You also want to take good care of your family and other loved ones by providing for them and helping set them up for rewarding lives of their own.

That’s a big reason why estate planning is vital for successful entrepreneurs who want to make certain that after their passing, their heirs and others have the financial resources they need to move ahead successfully in life.

At its core, estate planning is a process for how you transfer your wealth. When it’s done carefully and thoughtfully, estate planning can enable you to pass on your assets as you see fit—while minimizing the state and federal tax bills that often go along with the transfer of sizable wealth.

Chances are, you’re aware of that—and you may even have implemented an estate plan. But if you think that your current estate plan is set up to accomplish those tasks, you might want to think again.

Here’s why your estate plan may need to be revisited and revitalized—and, if so, how to make it happen.

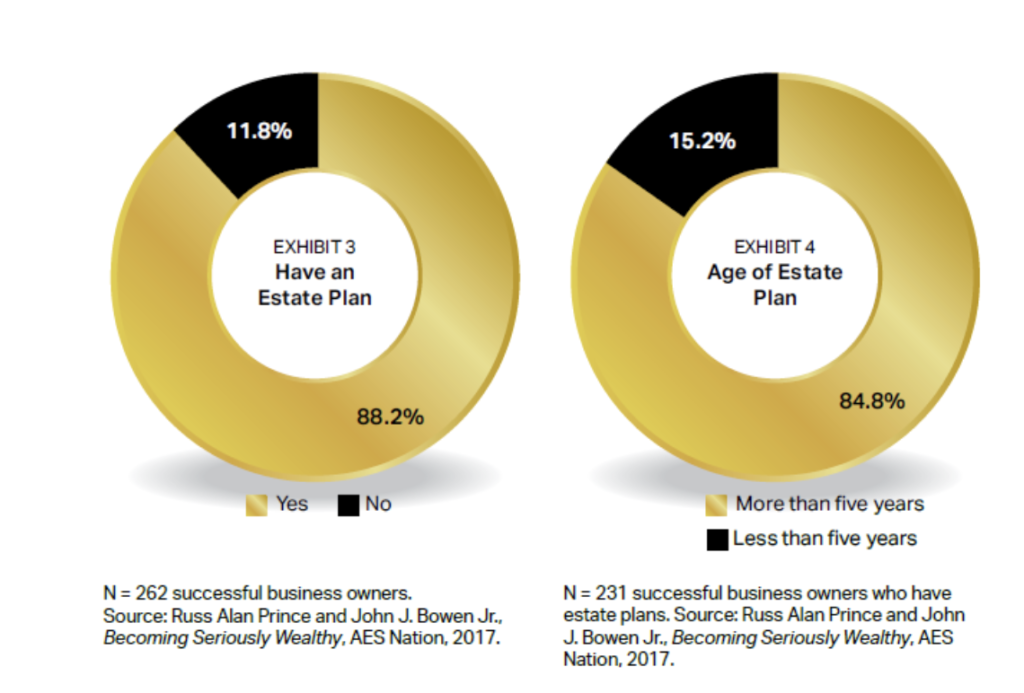

On the surface, it would seem that successful business owners are in good shape when it comes to planning for the eventual transfer of their estates. Consider that nearly nine out of ten business owners surveyed have an estate plan in place—which is defined as having, at a minimum, a will (see Exhibit 3). Having at least a will should help your loved ones avoid a great deal of trouble and stress when you pass on.

Unfortunately, a closer look reveals some troubling news: Entrepreneurs may not be nearly as well-prepared for wealth transfer as they think they are. Why? Because, we find, that approximately 85 percent of the estate plans that successful business owners have in place are more than five years old (see Exhibit 3 & 4).

That’s a potentially big problem—one that should raise a red flag that your plan could be outdated. Here’s why:

For example, consider that more than 60 percent of successful business owners report that they have become wealthier since they created their estate plans. Meanwhile, more than 75 percent say that they have experienced life-changing events since they created their estate plans.

These events—from divorce to the birth of children or grandchildren to the death of prospective guardians for minor children, and so forth—can have major impacts on planning for the future, and any existing estate plans.

The message is clear: It’s very likely that the current estate plans for a sizable number of successful business owners are outdated and ineffective. In order to attain the greatest benefits from estate planning, you need to stay on top of the matter and revise your estate plan when appropriate—especially as new events develop that potentially affect your company and your personal wealth.

When an estate plan is missing important elements or no longer reflects your wishes or your current situation, problems can quickly arise that may put your family’s financial future at risk. Consider these three examples:

So let’s say you’re among the roughly 85 percent of business owners with estate plans that are more than five years old. What steps should you take or consider taking?

Your first step should be to answer a few key questions, perhaps during a conversation with a trusted advisor or other professional:

If the answer to any of those questions is “yes,” it’s probably time to update your plan in some way. As you move forward with that mission, there are some important issues to consider that will help you assess and rethink your existing estate plan.

Start by determining the ideal outcome or outcomes of an estate plan, in your eyes. Distributing your assets at death as you want them to be distributed must be the No. 1 driver behind any estate-planning decisions. Knowing what you want to have happen to your wealth is foundational.

Warning: Don’t over-focus on how you can cut your estate tax bill by the maximum amount possible. That’s a big mistake. Some strategies that enable maximum tax benefits often come with strings attached that require you to entirely cede control of the assets you want to transfer—an outcome that may be highly undesirable to you. Remember, the true goal of estate planning is to transfer your wealth in accordance with your wishes. Tax mitigation, while often very important and beneficial, should not be the overriding driver of your estate-planning decisions.

Armed with this information, consider issues such as:

Pro tip: Documents that should be part of most estate plans include a basic will, trust documents, beneficiary forms for life insurance and investment/retirement accounts, durable power of attorney, health care power of attorney, living will (advance medical directive), inventory of assets, list of contacts (bankers, advisors, attorneys, etc.), list of passwords to email and other online accounts, and funeral arrangements.

This report was prepared by, and is reprinted with permission from, VFO Inner Circle. AES Nation, LLC is the creator and publisher of VFO Inner Circle reports.

Disclosure: The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra IS or Kestra AS. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by Kestra IS or Kestra AS for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment advisory services offered through Kestra Advisory Services, LLC (Kestra AS), an affiliate of Kestra IS.

Fusion Wealth Management is not affiliated with Kestra IS or Kestra AS. https://www.kestrafinancial.com/disclosures

VFO Inner Circle Special Report

By Russ Alan Prince and John J. Bowen Jr.

© Copyright 2021 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, includ- ing, but not limited to, electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the authors nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The authors will make recommendations for solutions for you to explore that are not our own. Any recommendation is always based on the authors’ research and experience.

The information contained herein is accurate to the best of the publisher’s and authors’ knowledge; however, the publisher and authors can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Unless otherwise noted, the source for all data cited regarding financial advisors in this report is CEG Worldwide, LLC. The source for all data cited regarding business owners and other professionals is AES Nation, LLC.